Use the data to review your business and work towards meaningful long-term improvement.

Subscribers to the Insurance Broker’s Code of Practice (the Code) complete a Compliance Statement each year detailing how they dealt with consumer complaints during the previous 12 months and the number of times when the Code was breached.

The Insurance Brokers Code Compliance Committee (the Committee), the independent body that monitors the Code, has begun analysing the 2019 data and presents a preliminary overview here. A complete report will be published later this year when the Committee publishes its Annual Review. The ACS is the key element of the Committee’s monitoring work.

Data and percentages are based on the 284 insurance broking companies subscribing to the Code in 2019.

Code breach data collected for 2019 indicates a rise in self-reported Code breaches over the previous year from 1,821 to 2,006, an increase of 10%. Given that self-reporting breaches is a sign of a healthy compliance framework, the Committee was encouraged to see that the percentage of breaches had risen and also noted that the number of subscribers self-reporting breaches rose to 51 per cent in 2019 from 43 per cent.

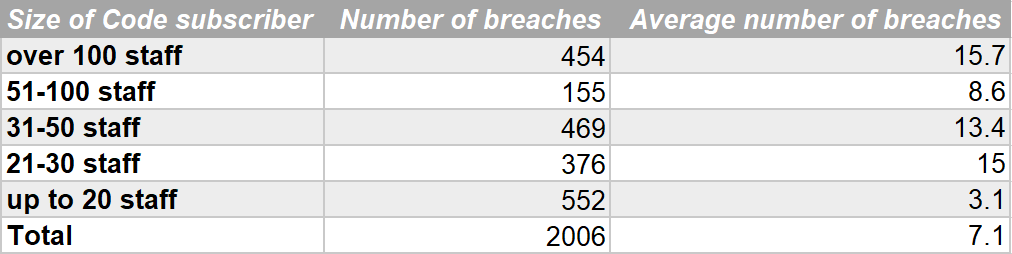

The number of breaches by Code subscriber size is detailed below. We also detail the average number of breaches per subscriber based on the size of the company.

The Committee is concerned that whilst 51% of subscribers reported breaches, 49% of subscribers reported Nil breaches.

This may indicate that many subscribers’ internal frameworks are not robust enough to identify Code breaches.

We urge Code subscribers reporting nil breaches to review their recording trigger points, assess their frameworks for recording complaints and breaches, monitor how these are recorded in practice, and to consider how staff are trained to identify Code breaches.

Whilst the Committee is yet to analyse the detailed breach data reports, we can report that the most self-reported breaches by far were associated with buying insurance (Service Standard 5), at 869 breaches or 43% of total breaches. The top three breaches which account for 80% of all breaches are detailed below:

- Buying insurance (Service Standard 5): 869 (or 43.3%) of self-reported Code breaches

- Legal obligations (Service Standard 1): 469 (or 23.4%) of self-reported Code breaches.

- Scope of covered Services (Service Standard 4): 269 (or 13.4%) of self-reported Code breaches.

- Money handling (Service Standard 7): 111 (or 5.5%) of self-reported Code breaches

- Professionalism (Service Standard 12): 100 (or 5.0%) of self-reported Code breaches.

Subscriber self-reported that 10,255 consumers were impacted by Code breaches, including a financial impact of over $1.2m.

The main root causes for Code breaches included process and procedures not followed and manual error.

In the area of complaints, 1,292 complaints were self-reported by subscribers, an increase of 23% over the 1,049 complaints reported in 2018. These came from 60 per cent of Code subscribers, with 108 Code subscribers reporting no complaints at all.

Of the complaints,463 (36%) related to poor claims service, similar to 2018. The percentage of complaints resolved within 21 days dropped slightly from the previous year, down from 63% in 2018 to 59%.

- 59% of complaints resolved within 21 days, down from 63% in 2018.

- 24% of self-reported complaints involved small business policies, up from 21% in 2018. 19% involved motor vehicle, split 10% for personal and 9% for commercial motor vehicle complaints. 8% involved Home Building complaints.

- 36% of self-reported complaints concerned poor claims service, similar to 37% in 2018.

- 18% of self-reported complaints concerned poor general service, down from 23% in 2018. 9% concerned incorrect advice and 7% concerned charges.

The Committee hopes these early insights will spark discussion about how Code subscribers are meeting the service standards set out in the Code. Addressing consumer concerns in a fair and reasonable way, making good practice integral to their business and embracing Code obligations not as a matter for technical compliance but as a crucial means of improving professional behaviour and enhancing service to clients.